{kind=link}

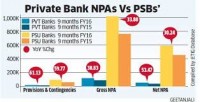

The details of Gross Advances, Gross Non-Performing Assets (GNPA) and Gross NPA ratio of Scheduled Commercial Banks (SCBs) and Public Sector Banks (PSBs) for last three years are as under:

| SCHEDULED COMMERCIAL BANKS (Rs. In crore) | |||

| GROSS ADVANCES | GNPA | GNPA RATIO | |

| FY 2014 | 61,01,775 | 2,51,060 | 4.11% |

| FY 2015 | 66,92,522 | 3,09,408 | 4.62% |

| FY 2016 | 72,86,952 | 5,41,763 | 7.43% |

| PUBLIC SECTOR BANKS (Rs. In crore) | |||

| GROSS ADVANCES | GNPA | GNPA RATIO | |

| FY 2014 | 45,90,458 | 2,16,739 | 4.72% |

| FY 2015 | 49,17,228 | 2,67,065 | 5.43% |

| FY 2016 | 51,16,985 | 4,76,816 | 9.32% |

Main reasons for increase in NPAs of banks are sluggishness in the domestic growth during the recent past, slowdown in recovery in the global economy and continuing uncertainty in the global markets leading to lower exports of various products like textiles, engineering goods, leather, gems, external factors including the ban in mining projects, delay in clearances affecting Power, Iron & Steel sector, volatility in prices of raw material and the shortage in availability of power have impacted the operations in the Textiles, Iron & steel, Infrastructure sectors, delay in collection of receivables causing a strain on various Infrastructure projects, aggressive lending by banks in past.

The government has taken specific measures to address issues in sectors such as Infrastructure (Power, Roads etc.), Steel and Textiles, where incidence of NPAs is high. The government has also approved establishment of six (6) new Debt Recovery Tribunals (DRTs), to speed up the recovery of bad loans of the banking sector, in addition to existing thirty three. Reserve Bank of India (RBI) has also undertaken steps which include (i) Formation of Joint Lenders’ Forum (JLF) for revitalising stressed assets in the system, (ii) Flexible Structuring for long term project loans to Infrastructure and Core industries, and (iii) Strategic Debt Restructuring (SDR) scheme. (iv) Scheme for Sustainable Structuring of Stressed Assets (S4A).The Government has recently issued advisory to banks to take action against guarantors in event of default by borrower under relevant sections of SARFAESI Act, Indian Contract Act & RDDB&FI Act, since in the event of default; the liability of the guarantor is co-extensive with the borrower.